%20Outline.png)

How to Accept Credit Cards Online: A Clear Guide for Business Owners

- Clarity

- Dec 24, 2025

- 15 min read

Updated: Dec 29, 2025

To accept credit cards online, you'll need to partner with a payment processor to set up two key components: a merchant account, which is a special bank account for holding transaction funds, and a payment gateway, the technology that securely connects your website to the payment networks.

The quickest way to get started is with an all-in-one Payment Service Provider (PSP) like Authorize.net. They bundle the merchant account and gateway into a single, easy-to-use service, which is ideal for new businesses that need to begin accepting payments quickly.

Your First Steps to Accepting Online Payments

Before diving into the technical details, it’s important to understand how money moves from your customer's card to your business bank account. Making the right choice at this stage can save you significant money and prevent operational headaches in the future.

At its core, every online credit card transaction requires two essential services:

A Merchant Account: This is not your standard business checking account. It's a specialized account designed to receive funds from credit and debit card sales before they are transferred to your primary bank account.

A Payment Gateway: Think of this as your website's virtual credit card terminal. It's the secure software that encrypts a customer's card details, sends the information to the payment networks for approval, and communicates back to your website whether the payment was successful.

You must have both. The key decision is how you obtain them.

The Two Main Paths for Online Processing

You have two primary options for setting up your online payment infrastructure.

One path is to use a Payment Service Provider (PSP), sometimes called an aggregator. Well-known examples include Stripe, PayPal, and Square. They combine the merchant account and payment gateway into a single package with straightforward, flat-rate pricing. This makes them an excellent choice for new businesses, startups, or merchants with lower sales volumes who prioritize simplicity and speed.

The other route is to establish a dedicated merchant account directly with a payment processor. This approach keeps the merchant account and payment gateway as separate components, offering greater control, long-term stability, and more transparent pricing models like Interchange-Plus. The application is more detailed because a human underwriter assesses your business's specific risk profile. However, the result is a stable and often more cost-effective solution designed for established or high-volume businesses.

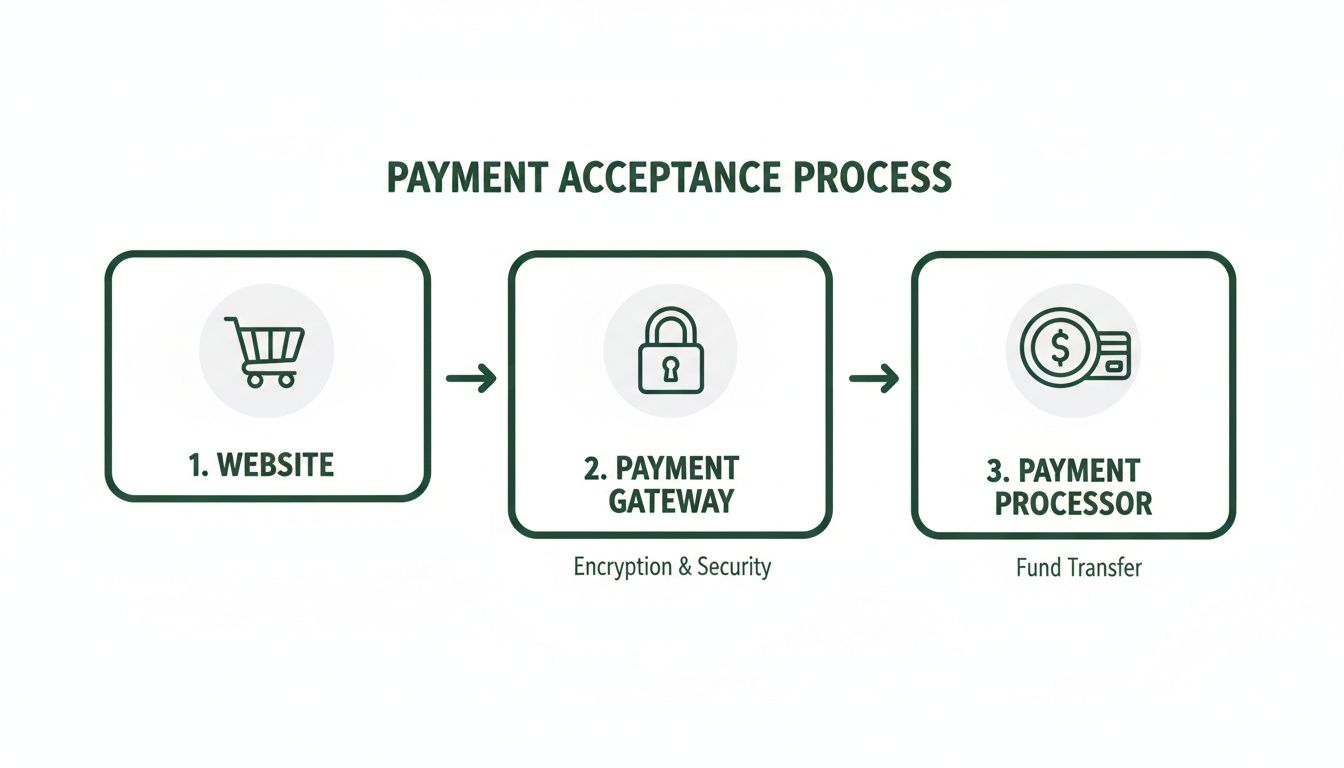

Here’s a simple visual of how a transaction flows from your website to the processor.

As you can see, the gateway acts as the critical messenger, handling the secure communication between your website and the financial networks.

To make the choice clearer, here’s a side-by-side look at how these two models compare.

Payment Service Provider vs. Dedicated Merchant Account

This table breaks down the key differences to help you decide which model is the right fit for your business, focusing on stability, cost, and the support you can expect.

Feature | Payment Service Provider (e.g., Stripe, PayPal) | Dedicated Merchant Account |

|---|---|---|

Setup Speed | Very fast (often same-day approval) | Slower (1-3 days due to underwriting) |

Pricing Model | Simple flat-rate (e.g., 2.9% + 30¢) | More transparent, often lower cost (e.g., Interchange-Plus) |

Account Stability | Lower; accounts can be frozen or terminated with little warning | High; dedicated underwriting provides long-term stability |

Best For | Startups, low-volume businesses, simplicity seekers | Established businesses, high-volume merchants, high-risk industries |

Support | Often email or chat-based, can be slower | Typically a dedicated account manager and phone support |

Ultimately, a dedicated account offers a more robust, personalized foundation, while a PSP provides unmatched speed and simplicity for getting started.

Why This Initial Choice Matters So Much

Choosing between a PSP and a dedicated merchant account is more than a technical decision—it has significant implications for your business's financial health and stability.

For instance, if you operate in an industry considered "high-risk"—such as CBD, subscription boxes, or credit repair—a PSP is often a risky choice. Their terms of service are typically rigid, and you face a real risk of having your account suddenly frozen or terminated if their automated systems flag your activity. This can halt your revenue stream without warning.

For any business in a regulated or high-chargeback industry, a dedicated high-risk merchant account is essential for stability. The upfront underwriting process ensures the processor understands your business model from the start, drastically reducing the risk of sudden account holds that can disrupt your cash flow.

Today, your customers expect to pay by card. In 2025, it’s a standard business requirement. The US already has a 94% credit card acceptance rate among merchants. If you're running an ecommerce store without a reliable method for accepting card payments, you're invisible to a large portion of your potential market.

To learn more about setting up a reliable system, you can explore the fundamentals of online payments and understand why a stable infrastructure is key to growth.

Choosing and Integrating Your Payment Gateway

A payment gateway is the digital equivalent of a physical credit card terminal. It’s the secure technology that connects your website to your payment processor, ensuring your customer’s sensitive financial data is transmitted safely and instantly.

How you integrate this technology into your site is a crucial decision. It involves balancing the desired customer experience, your team's technical capabilities, and the level of security responsibility you are prepared to assume. Let's review the three primary integration methods.

Hosted Checkout Pages

For most businesses, especially those just starting, a hosted checkout page is the simplest and most secure option. When a customer clicks "Pay Now," they are redirected from your website to a secure payment page hosted by your payment provider.

After entering their card details and completing the payment, they are sent back to your website for confirmation. Because sensitive data never touches your servers, your PCI DSS compliance requirements are significantly reduced. This is an ideal choice if you do not have a developer on your team, as the setup is typically very straightforward.

The upside: It greatly simplifies PCI compliance and is quick to implement, often with minimal coding.

The downside: The customer temporarily leaves your website, which can disrupt a carefully designed brand experience.

For example, a small artisan shop using a basic website builder can use this method to add a "Buy Now" button that directs customers to a trusted payment page, eliminating the need to become a security expert.

Direct API Integration

If you want complete control over the checkout process and a seamless brand experience, a direct API (Application Programming Interface) integration is the best solution. An API allows your website's software to communicate directly with the payment gateway, so the entire transaction occurs on your domain.

This gives you the freedom to design a fully custom checkout flow that matches the look and feel of your site. Customers never leave, which can build trust and improve conversion rates. However, this control comes with significant responsibility.

A direct API means you are handling sensitive cardholder data. This places a much greater PCI compliance burden on your business. You must ensure your systems are highly secure, a task that requires substantial technical expertise and ongoing maintenance.

A subscription box company is a good example of a business that would benefit from an API. It enables them to create a polished, frictionless sign-up process and securely store payment tokens for recurring billing, all without redirecting the customer off-site. You can explore a variety of gateway services to find one that offers the API features your business model requires.

E-commerce Plugins and Extensions

If your store runs on a popular platform like Shopify, WooCommerce, or BigCommerce, integration is much simpler. The easiest path is to use a dedicated plugin or extension. These platforms have large marketplaces filled with pre-built integrations for nearly every major payment gateway.

Setup is usually simple—often requiring just a few clicks in your admin dashboard. You select your provider, install their official plugin, and enter your account credentials. The plugin handles the complex connections and security protocols for you.

This approach offers an excellent middle ground. You get a smooth, on-site checkout experience (many plugins use embedded forms) without the technical complexity or security responsibilities of a full API integration. It's the preferred choice for millions of online stores for good reason.

Decoding Pricing Models and Hidden Fees

Confusing payment processing fees can quickly erode your profits. This is one of the most common areas where business owners face challenges, often accepting unfavorable terms because the pricing structure was not clear.

Let's clarify the terminology. Understanding how you are charged is the single most important factor in choosing a partner to accept credit cards online.

The Three Core Pricing Models Explained

To illustrate, let's use a $100 transaction and see how the actual cost varies with each model. This will highlight why some structures are transparent while others can conceal additional markups.

Flat-Rate Pricing: This is the simplest model, used by providers like Stripe and PayPal. You are charged a single, predictable percentage plus a small fixed fee for every transaction, such as 2.9% + $0.30. * On a $100 sale: Your cost is ($100 0.029) + $0.30 = $3.20. * The trade-off: This is ideal for startups and small businesses that need predictable costs. You pay a premium for the simplicity, but there are no surprises on your statement.

Tiered Pricing: This is where pricing can become less clear. Processors group hundreds of different card types into a few categories, typically named "Qualified," "Mid-Qualified," and "Non-Qualified." The processor determines which tier each transaction falls into. * On a $100 sale: A standard debit card might receive the low "Qualified" rate of 1.69% (costing you $1.69), but a customer using a corporate rewards card could be downgraded to the "Non-Qualified" tier at 3.50% (costing you $3.50). It is often difficult to understand why the costs differ. * A word of caution: This model is known for its lack of transparency. It makes it nearly impossible to forecast costs accurately and allows processors to increase their profits by downgrading transactions into more expensive tiers.

Interchange-Plus Pricing: Also known as "cost-plus," this is the most transparent pricing available and is the standard for businesses with established sales volume. It works by passing the direct wholesale cost (the "interchange" rate set by card brands like Visa and Mastercard) directly to you and adding a small, fixed markup. * On a $100 sale: Let’s say the wholesale interchange rate for the card used is 1.43% + $0.10. If your processor’s markup is 0.25% + $0.10, your total cost would be (1.43% + 0.25%) + ($0.10 + $0.10) = 1.68% + $0.20. Your total cost is $1.88. * Your monthly statement will clearly separate the interchange cost and the processor's markup, providing full transparency.

The key benefit of Interchange-Plus is transparency. You see the true cost you’re paying to the card brand and the exact, predictable fee your processor earns. There is no room for hidden markups in the transaction rate itself.

Comparing Online Payment Pricing Models

This table provides a quick breakdown of the three main pricing structures to help you visualize the differences. It illustrates how costs are calculated and highlights which model offers the most transparency for your business.

Pricing Model | How It Works | Best For | Potential Downsides |

|---|---|---|---|

Flat-Rate | A single, predictable percentage and a fixed fee are charged on every transaction (e.g., 2.9% + $0.30). | Startups and small businesses that prioritize simplicity and predictability. | Higher effective rates as sales volume grows; you overpay on low-cost card types. |

Tiered | Transactions are grouped into 2-3 "tiers" (e.g., Qualified, Non-Qualified), each with a different rate set by the processor. | Businesses that have not yet been offered a more transparent model. | Lacks transparency, results in unpredictable costs, and allows for hidden markups. |

Interchange-Plus | Passes the true wholesale interchange cost directly to you and adds a small, pre-negotiated markup from the processor. | Established businesses and anyone wanting full transparency and lower costs. | Statements are more detailed, which may seem complex initially. |

While Flat-Rate pricing is excellent for getting started, Interchange-Plus is the goal for a growing business to ensure you receive the most fair and transparent rates.

Uncovering Common Hidden Fees

Beyond the per-transaction rate, your monthly statement can contain additional charges. Knowing what to look for is essential to understanding your true cost of accepting payments.

Use this checklist when evaluating processors and reviewing your monthly statements. These are fees that are not always advertised upfront:

Monthly Fee / Account Fee: A standard charge for maintaining your account.

Monthly Minimum Fee: A penalty applied if your transaction fees do not reach a specified amount for the month.

PCI Compliance Fee: A fee for maintaining Payment Card Industry security standards. Some processors charge a higher "non-compliance" fee if you fail to complete your annual validation.

Batch Fee: A small fee charged each time you settle your daily transactions.

Chargeback Fee: A penalty, often $25-$50, charged each time a customer disputes a transaction—even if you win the dispute.

The global shift to digital payments is accelerating. Non-cash transaction volumes are projected to reach 1,650.5 billion in 2024. In a major market like Canada, credit cards already account for 46% of all e-commerce payments. This trend underscores the importance of securing a clear fee structure. To see how these trends are shaping different markets, review the latest online payment statistics from Airwallex. The data shows that as your online sales grow, a transparent pricing model becomes a necessity.

Navigating Security, PCI Compliance, and Fraud

When you accept credit cards online, you are not just processing payments—you are responsible for protecting sensitive financial data. Fulfilling this responsibility is fundamental to earning customer trust and protecting your business from significant financial and reputational damage.

At the center of this is the Payment Card Industry Data Security Standard (PCI DSS). This is a set of security rules created by the major card brands (Visa, Mastercard, American Express, etc.) that every business accepting card payments must follow. Its purpose is to secure cardholder information and prevent data breaches.

Understanding Your PCI Compliance Responsibilities

Your level of PCI compliance responsibility is determined by how you integrate your payment gateway. The less your systems "touch" raw card data, the simpler your compliance tasks will be.

Hosted Checkout Pages: This is the most straightforward path. If your customers are redirected to a payment page hosted by your provider (like Stripe Checkout or PayPal), your PCI responsibilities are minimal. The gateway handles the security, and you will likely only need to complete a simple self-assessment questionnaire annually.

API Integrations: If you build a custom checkout form directly on your site using an API, your responsibilities increase significantly. Because card data passes through your systems, you must prove that your entire network is secure. This may require more complex assessments and mandatory network scans.

Ignoring these regulations is a poor business decision. Processors can impose steep monthly non-compliance fees until you become validated. More importantly, if a data breach occurs, the resulting fines can be financially devastating.

Your primary security goal should be to reduce your "PCI scope" as much as possible. Choose an integration method that prevents raw credit card numbers from ever touching your servers. This single step will drastically reduce your security workload and risk.

Essential Fraud Prevention Tools

In addition to preventing data breaches, you must also prevent fraudulent transactions. A high number of fraudulent orders leads to an increase in chargebacks, which can jeopardize your merchant account.

Fortunately, modern payment gateways include a built-in suite of tools to detect fraudulent transactions. Before selecting a provider, ensure they offer these essential features:

Address Verification Service (AVS): This is a basic but effective check that confirms whether the billing address entered by the customer matches the address on file with the card-issuing bank. A mismatch is a common indicator of fraud.

Card Verification Value (CVV): Requiring the three- or four-digit code from the back of the card helps verify that the customer is in physical possession of the card.

3D Secure (e.g., Verified by Visa, Mastercard SecureCode): This adds an extra layer of authentication. After entering their card information, the customer is prompted by their bank to enter a password or a one-time code sent to their phone, confirming their identity.

Tokenization: Your Best Friend in Data Security

One of the most important security technologies is tokenization. The concept is simple but highly effective.

When a customer makes a payment, the gateway encrypts their card number and replaces it with a unique, randomly generated string of characters—a "token."

You can then store this token for recurring subscriptions or saved customer profiles. The actual credit card number is stored securely in your processor's vault, never touching your systems. If a hacker were to breach your database, they would only find useless tokens, not valuable financial data.

Security is not an area for shortcuts. It is about building a trustworthy business and ensuring you can continue to accept payments reliably for years to come. For more details on how data is handled, always review your provider's policies, such as our comprehensive privacy policy.

Special Considerations for High-Risk and B2B Businesses

Not all businesses fit the standard mold for payment processing. If you operate in an industry deemed "high-risk" or primarily sell to other businesses (B2B), a specialized approach to accepting credit cards online is necessary. Standard, one-size-fits-all providers are often not equipped to handle your needs, which can lead to significant problems.

The Truth About "High-Risk" Processing

First, it is important to understand what "high-risk" means. This label is not a judgment on your business practices. It is an internal classification used by processors for industries that historically experience higher chargeback rates or operate in legally complex sectors. This includes businesses in industries like CBD, nutraceuticals, subscription boxes, and credit repair.

Using a generic PSP like Stripe or PayPal for these industries is a gamble. Their automated systems may approve you initially, but a small increase in chargebacks or a manual review of your business model could lead to a sudden account freeze or termination. This can halt your cash flow instantly, forcing you to find a new payment solution under pressure.

Finding a processor that openly specializes in your industry is crucial for long-term stability. These partners understand the nuances of your business and conduct thorough upfront underwriting to ensure they can support you reliably as you grow.

To find the right partner, seek out providers who have demonstrated expertise in high-risk merchant accounts. These specialists are prepared for your industry's unique challenges and provide the account stability you need.

How B2B Payment Processing is Different

Business-to-business (B2B) payments have unique requirements. Transactions typically involve larger amounts and corporate purchasing cards, which are processed differently than consumer credit cards. The key to optimizing B2B payments is to provide more detailed data with each transaction.

This is where Level 2 and Level 3 data processing becomes important. By submitting additional information with a transaction—such as a customer code or invoice number—you can qualify for significantly lower interchange rates from Visa and Mastercard. Over time, these savings can be substantial.

For B2B companies that accept orders over the phone or via email, a virtual terminal is an essential tool. It is a secure webpage provided by your processor that allows you to manually enter a customer's credit card details. This turns any computer into a secure credit card terminal, perfect for handling mail order/telephone order (MOTO) payments without additional hardware.

Unlocking Growth in Specialized Markets

Success in these specialized markets requires staying informed about payment trends and card network requirements. For example, commercial card usage is a major driver of B2B online payments, yet research from Mastercard shows 1 in 4 businesses are blocked from cross-border transactions due to fraud concerns.

The use of virtual cards for business is expected to reach $500 billion in 2025, highlighting the importance of having a B2B processor that can handle modern payment methods. By offering options like American Express, which accounts for 19% of US card volume, you can better serve your corporate clients. You can explore these trends further with these insightful credit card statistics.

Whether you are in a high-risk industry or the B2B space, the right processing partner is more than a service provider. They are a stable, specialized foundation you need to protect your revenue and scale your business with confidence.

Common Questions About Accepting Payments Online

As you prepare to accept credit cards online, several practical questions will likely arise. Getting clear answers from the start can help you avoid future complications. Here are some of the most common inquiries from business owners setting up online payment processing.

How Long Does It Take to Get Approved?

The timeline for approval depends directly on the type of provider you choose and the depth of their upfront risk assessment.

All-in-one platforms like Square or PayPal are known for instant or same-day approvals. They achieve this speed by using an aggregated model, where they process transactions under their own master merchant account. While this speed is convenient, it comes with a trade-off: their detailed underwriting often occurs after you have started processing payments. This can lead to unexpected account freezes or terminations if they later determine your business does not meet their risk criteria.

In contrast, applying for a dedicated merchant account involves a more thorough upfront review. A human underwriter examines your business, website, and sales history. This process typically takes 24 to 72 hours. This initial diligence creates a much more stable, long-term processing relationship because the provider fully understands your business model from the outset. For any business with significant sales volume or in a high-risk category, this stability is invaluable.

What Is a Chargeback and How Do I Prevent It?

A chargeback is a transaction reversal initiated by a customer who disputes a charge with their bank. It is a consumer protection mechanism that can become a major issue for merchants, costing not only the sale amount but also a penalty fee of $25 or more.

Your chargeback ratio—the number of chargebacks compared to your total transactions—is a key health indicator for your merchant account. If it rises too high (typically above 1%), processors may terminate your account to limit their financial risk.

The most effective way to manage chargebacks is to prevent them. This comes down to proactive communication and clear business policies. Here are a few immediate steps you can take:

Use a Clear Billing Descriptor: Ensure the name that appears on your customer's credit card statement is easily recognizable as your business. Confusion is a leading cause of chargebacks.

Provide Excellent Customer Service: Make it easy for customers to contact you to request a refund. A simple refund is always preferable to a chargeback.

Utilize Fraud Prevention Tools: Always require the CVV code and use the Address Verification Service (AVS) to help identify suspicious transactions before they are processed.

Can I Use One Account for My Website and Store?

Yes, and for businesses with both a physical and online presence, this is often the most efficient approach. A quality payment processor can provide an omnichannel solution, which links a single merchant account to both your e-commerce payment gateway and your in-store point-of-sale (POS) system.

This centralized setup simplifies your operations. It makes bookkeeping easier, helps streamline inventory management, and provides a holistic view of your customers' purchasing behavior across all channels. Additionally, by consolidating your total transaction volume with a single provider, you can often negotiate better pricing.

What Is a Virtual Terminal and Do I Need One?

A virtual terminal is a secure webpage that allows you to manually enter credit card information from any computer with an internet connection. It effectively turns your laptop or desktop into a credit card terminal without requiring any special hardware.

If you ever accept payments over the phone or by mail—known as Mail Order/Telephone Order (MOTO) transactions—a virtual terminal is essential. This makes it a critical tool for B2B companies, service-based businesses, and anyone who takes orders where the customer's card is not physically present. Most dedicated merchant accounts include a virtual terminal as a standard feature.

For more detailed answers to specific payment questions, our extensive FAQ page is a great resource to have on hand.

Navigating the world of online payments requires a partner focused on clarity and stability. At Clarity Merchant, LLC, we help businesses establish transparent, reliable processing solutions built for the long haul. Learn how we can support your business today.

Comments